A lot of first-home buyers are trying to make good decisions while everyone around them is speaking bank, legal and property nonsense.

LVR. Servicing. Cash to complete. Formal approval. Valuation. Settlement.

None of these words are that complicated once someone explains them properly. But when you are hearing them for the first time, they can make the whole process feel more confusing than it needs to be.

So here is a plain-English translation guide for common terms first-home buyers usually need to understand early. It is a long one, so skim to the section that matches where you are in the process.

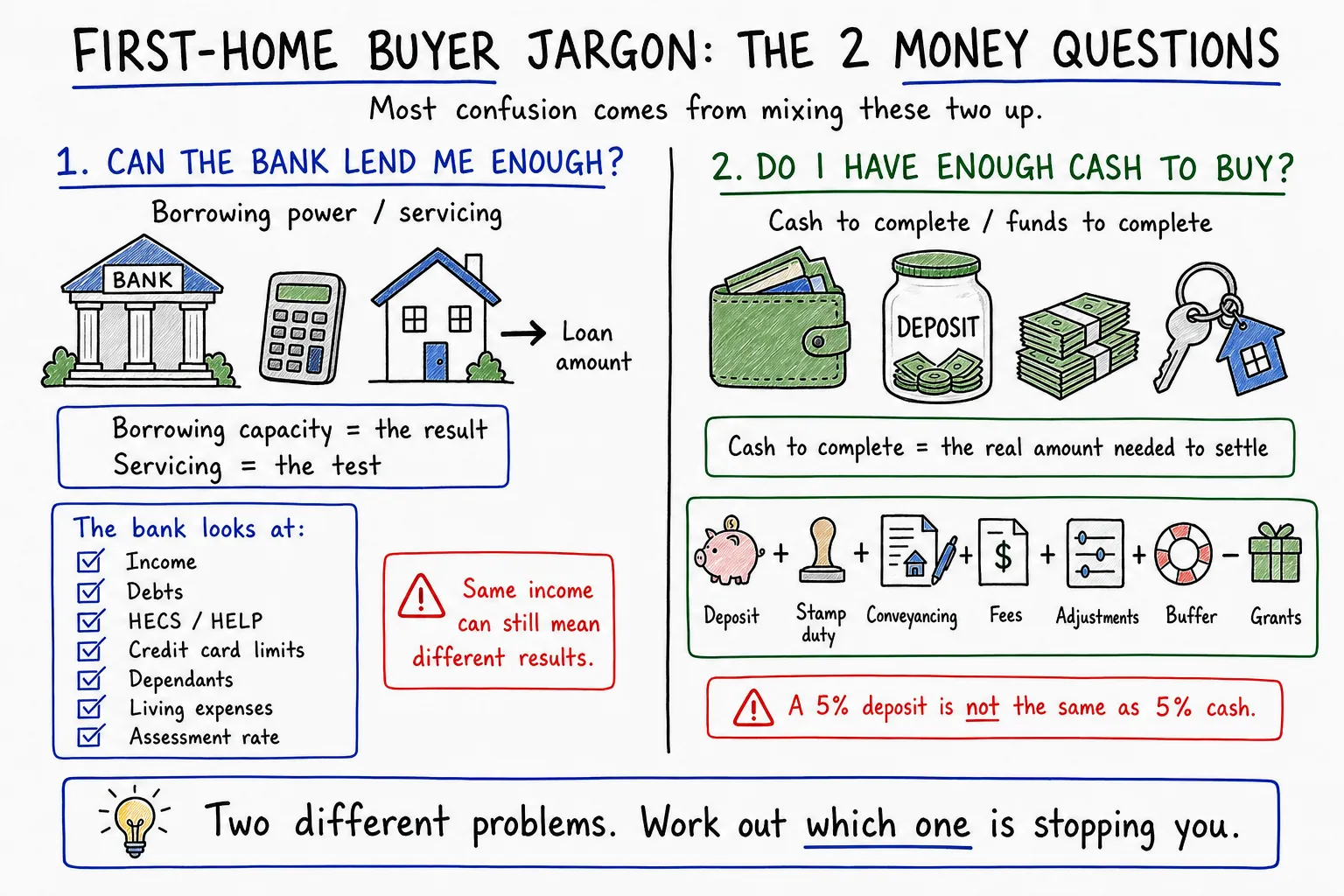

1. Can the bank lend me enough?

This is the borrowing power side of the equation. You might have a good deposit, but if the bank does not think the loan is affordable, the loan amount still may not work.

Borrowing capacity / servicing

Borrowing capacity is how much the bank thinks you can afford to borrow. Servicing is the calculation they use to work that out.

The bank looks at your income, debts, HECS, credit cards, dependants, living expenses and the new loan you are applying for.

This is why two people on the same income can get very different borrowing capacity results. One might have no debts, no kids and no HECS. The other might have a car loan, two credit cards and a dependant. Same income. Very different bank assessment.

I have written about this in more detail in Deposit and borrowing power are not the same thing.

Assessment rate

The assessment rate is the higher interest rate the bank uses to test your loan.

You might be applying for a loan with an actual rate around 6%, but the bank may test your affordability at a much higher rate after adding a buffer. This is why people sometimes say, "But I can afford the actual repayment."

The bank is not only testing whether you can afford today's repayment. They are testing whether the loan still works if rates are higher. That is one reason borrowing capacity can feel more conservative than people expect.

HECS, credit cards and other debts

These are not really jargon, but they matter a lot.

A HECS debt can reduce your usable income because the lender factors in the compulsory repayment.

A credit card can hurt borrowing power even if you pay it off every month, because lenders usually assess the limit, not just the balance. A $10,000 credit card with nothing owing can still reduce borrowing capacity.

Car loans, personal loans and buy now pay later commitments can also make a difference because they are existing repayments the bank has to allow for before adding a home loan. This is where people get caught out. They focus on income, but the bank is looking at income after commitments.

2. Do I have enough cash to actually buy?

This is separate from borrowing capacity. Some buyers can borrow enough, but do not have enough cash to complete the purchase. Other buyers have a strong deposit, but cannot borrow enough.

They sound connected, but they are not always the same problem.

Deposit

Your deposit is the part of the purchase price you are contributing yourself. If you buy for $700,000 and put in $70,000, that is a 10% deposit. But your deposit is not the same thing as the total cash you need.

This is probably one of the biggest first-home buyer traps. People hear "5% deposit" and think that means 5% is all they need. Usually, it is not. You still need to think about stamp duty, conveyancing, building and pest, bank fees, government fees, settlement adjustments, moving costs, insurance and some money left over.

I have written more about that in The hidden costs first-home buyers forget.

LVR

LVR means loan-to-value ratio. It is just the percentage of the property value you are borrowing.

If you buy for $700,000 and borrow $630,000, that is a 90% LVR. If you borrow $560,000 on the same property, that is an 80% LVR.

LVR matters because it can affect your interest rate, whether you pay lenders mortgage insurance, and which lenders or schemes are available to you. A lower LVR is usually stronger from the bank's point of view.

But a lower LVR does not automatically mean the bank will lend you more. It mainly helps with the deposit and risk side. You still need to pass servicing.

LMI

LMI stands for lenders mortgage insurance.

The annoying thing is that it protects the lender, not you. It usually comes up when you borrow more than 80% of the property value, unless you qualify for a waiver or a government scheme.

For example, if you buy with a 10% deposit, you may still have LMI because the bank is lending 90% of the property value.

LMI is not automatically good or bad. Sometimes paying LMI lets someone buy years earlier. Sometimes waiting and saving more makes more sense.

The main thing is understanding what it is, instead of thinking it is some random insurance policy protecting you.

Cash to complete / funds to complete

Cash to complete means the total amount of money you need to actually settle the purchase.

It includes your deposit, stamp duty, conveyancing, bank fees, government fees, settlement adjustments and other purchase costs. Then you subtract any grants, concessions or schemes that apply.

So if someone says, "I have a 5% deposit," that is only part of the story. The better question is: after all costs are included, do you actually have enough money to settle?

This number matters because it is possible to technically have the deposit, but still be short on the full cash required. If you want to see your own number, my free cost to complete calculator estimates it for any state and price point.

Stamp duty / transfer duty

Stamp duty, or transfer duty, is a state government tax on buying property. The amount depends on the state, the purchase price, whether you are a first-home buyer, whether you are buying to live in or invest, and what concessions apply.

Some first-home buyers pay none. Some pay a reduced amount. Some pay the full amount. This needs to be checked early because it directly affects your cash to complete. If you assume you are exempt and you are not, the numbers can change very quickly.

Genuine savings

Genuine savings usually means money you have saved or held over time, rather than money that appeared yesterday.

Different lenders have different rules around this. Some want to see that you have held a certain amount for at least three months. Some are more flexible depending on rent history, gifts, grants or other factors. This matters most when you are buying with a smaller deposit.

A buyer might have enough cash overall, but the lender may still ask where it came from and whether it meets their genuine savings policy.

Settlement adjustments

Settlement adjustments are small adjustments made at settlement for things like council rates, water, body corporate fees or rent if the property is tenanted.

Basically, the buyer and seller adjust who is responsible for which costs from settlement day. It is not usually the biggest cost in the world, but if your funds are tight, it can still matter. This is one reason I do not like buyers using every dollar just to get into the property.

Buffer

Buffer just means money left over after settlement.

This is not really bank jargon. It is more common sense. You generally do not want to use every dollar you have just to get the keys. Things break. Moving costs money. Insurance starts. Furniture exists. Life continues immediately after settlement, annoyingly.

A bigger buffer gives you more breathing room.

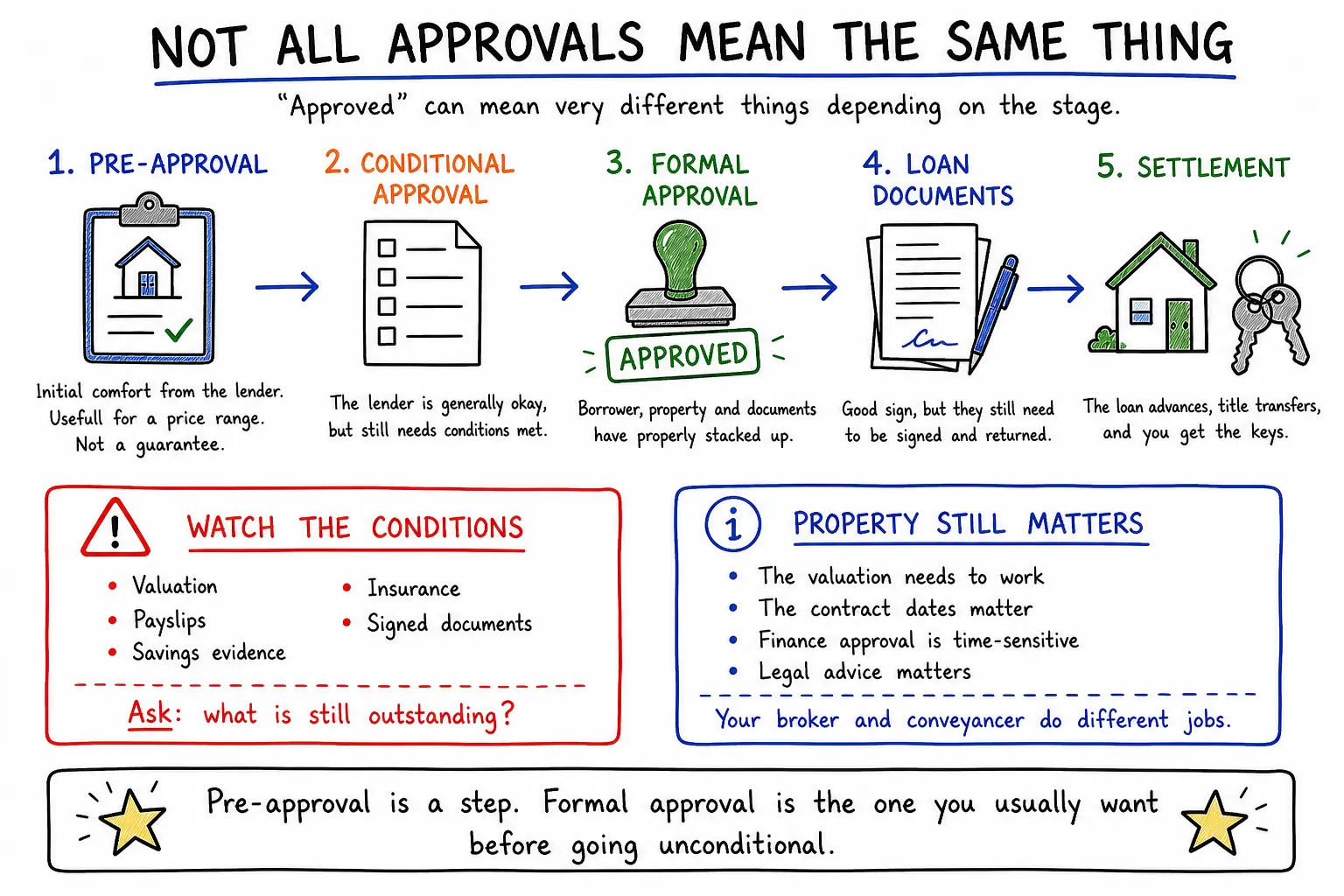

3. Am I actually approved yet?

This is where the word "approved" gets thrown around too casually.

Not all approvals mean the same thing. A pre-approval is not the same as formal approval. Conditional approval is not the same as being fully approved and ready for settlement.

Pre-approval

Pre-approval means the lender has had an initial look at your situation and is comfortable enough to give a conditional approval.

It can be useful because it gives you a clearer price range before you start seriously making offers. But it is not a guarantee.

The property still needs to be acceptable, the valuation needs to work, and your documents still need to stack up when the full application is assessed. Pre-approval is a good step. It is not a golden ticket.

Conditional approval

Conditional approval means the lender is generally okay with the loan, but still needs certain things checked or provided.

That might be a valuation, updated payslips, evidence of savings, insurance, signed documents or clarification around something in the application. Conditional approval is progress, but it is not the finish line.

The key question is: what conditions are still outstanding? Some conditions are easy. Some are more serious.

Formal approval / unconditional approval

Formal approval, or unconditional approval, is the stronger approval.

It generally means the lender is happy with the borrower, the property and the documents. If you have a finance clause in your contract, this is usually the approval you want before going unconditional on the purchase.

Different lenders and brokers may use slightly different wording, but the practical point is the same: this is when the bank has properly approved the deal.

Valuation

A valuation is the lender's assessment of the property value.

Often it matches the contract price, especially for a normal purchase. But not always. If the valuation comes in lower than the purchase price, it can create problems because the lender may base the loan on the lower value, not what you agreed to pay.

For example, if you buy for $700,000 but the bank values it at $680,000, the bank may use $680,000 for their LVR calculation. That can mean you need to contribute more cash or restructure the deal.

Loan documents

Loan documents are the formal documents you sign after approval.

They set out the loan amount, rate, repayments, security property, fees and other loan terms. Getting loan documents is a good sign, but the deal is not done just because they have been issued.

They still need to be signed, returned and certified properly before settlement can happen. This is where delays can happen if people leave things too late.

4. What happens after I sign a contract?

This is the legal and settlement side. Your broker handles the finance side. Your conveyancer or solicitor handles the legal side.

Finance clause

A finance clause is a condition in the contract that gives you time to get finance approved.

This matters a lot. If finance is not approved by the due date, your conveyancer can usually help you request an extension or terminate under the clause if needed.

The finance clause is basically one of the key protections for buyers, but it only works properly if you understand the dates and get advice before making decisions.

Do not rely on internet comments for contract advice here. Speak to your conveyancer before signing anything.

Building and pest

Building and pest is an inspection of the property before you fully commit.

It can pick up things like termites, water damage, structural issues, roof problems or other defects. It does not mean every small issue kills the deal. But it gives you more information before you go unconditional.

Sometimes the report gives peace of mind. Sometimes it gives you a reason to renegotiate. Sometimes it tells you to walk away.

Going unconditional

Going unconditional means the contract conditions have been satisfied or waived. At that point, you are usually properly committed to the purchase.

This is why you want to be very careful before going unconditional without finance approval or legal advice. It is one of those phrases that sounds harmless until you realise how serious it is. Once you are unconditional, changing your mind can get very expensive.

Conveyancer / solicitor

This is the person handling the legal side of the purchase.

They review the contract, explain your obligations, communicate with the seller's side, help manage settlement and make sure the property is transferred into your name.

A broker is not a substitute for a conveyancer. A conveyancer is not a substitute for a broker. They are doing different jobs, and both matter.

Settlement

Settlement is the day the property officially changes hands. The bank advances the loan, the seller gets paid, the title transfers, and you become the owner.

This is usually when you get the keys, although the exact timing can depend on the agent and settlement process. Settlement is the finish line of the purchase process, but it is also the start of actually owning the thing.

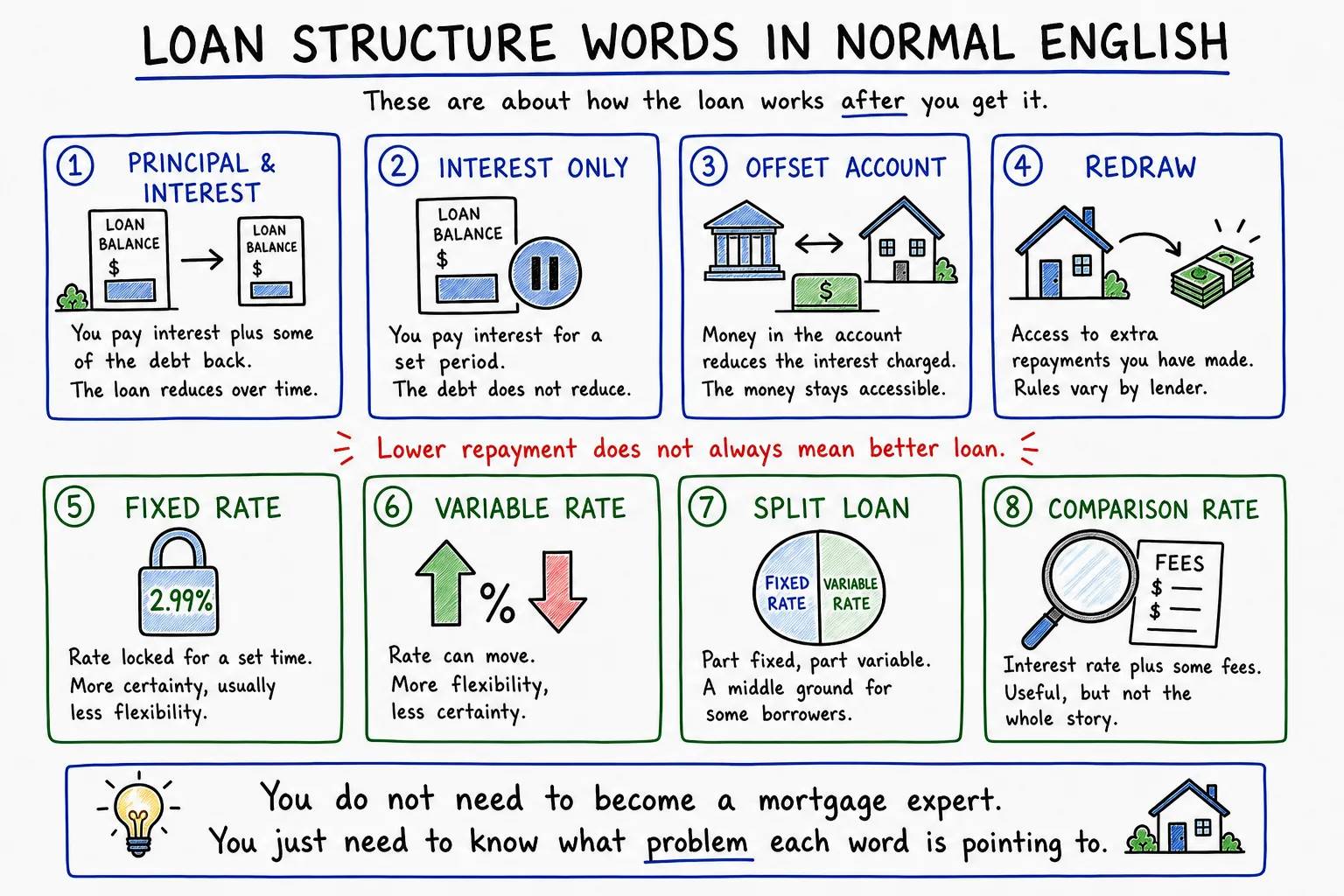

5. Loan structure words you might hear

These are not always the first thing to worry about, but they come up a lot.

This section is more about how the loan works after you get it.

Principal and interest

Principal and interest means your repayment includes interest plus some repayment of the loan balance. Over time, the debt reduces.

This is the standard setup for most owner-occupied first-home buyer loans. The repayment is higher than interest only, but you are actually paying the loan down.

Interest only

Interest only means you are only paying the interest for a set period. The loan balance does not reduce during the interest-only period.

This can make repayments lower in the short term, but it is not just a cheaper version of the same loan.

At some point, the loan either needs to switch back to principal and interest, be extended, refinanced or dealt with in some other way. It can make sense in some situations, but you want to understand the trade-off.

Offset account

An offset account is a transaction account linked to your home loan. Money sitting in the offset reduces the loan balance you pay interest on.

For example, if you have a $600,000 loan and $50,000 in offset, you are charged interest as if you owed $550,000.

The money is still accessible, which is why a lot of people like offsets for savings and emergency funds. It gives you interest savings without locking the money away.

Redraw

Redraw is access to extra repayments you have made into the loan.

If your minimum repayment is $3,000 and you pay extra over time, you may be able to redraw some of those extra repayments later.

It can be useful, but it is not always the same as an offset account. The rules can vary depending on the lender and product, so you want to understand how your specific loan works.

Fixed rate

A fixed rate means your interest rate is locked in for a set period.

This can give more certainty because your repayment does not move around during the fixed period. The trade-off is usually less flexibility. There may be limits on extra repayments, offset may be limited or unavailable, and break costs can apply if you exit the fixed loan early.

Variable rate

A variable rate can move up or down. This means your repayment can change when rates move.

The upside is usually flexibility. Variable loans often have better access to offset, redraw, extra repayments and refinancing.

The downside is less certainty. If rates increase, your repayment can increase too.

Split loan

A split loan means part of your loan is fixed and part is variable. Some borrowers use this because they want a bit of certainty on one part and flexibility on the other.

For example, they might fix half the loan and keep the other half variable with an offset account. It is not magic, but it can be a useful middle ground.

Comparison rate

The comparison rate tries to show the interest rate plus certain fees and charges.

For example, it might be based on a loan amount or loan term that does not match your actual situation. So do not ignore it, but do not treat it as the only thing that matters either. A loan with the lowest comparison rate is not automatically the right loan for every borrower.

Once you translate the jargon

The main thing with all of this is that you do not need to become a mortgage expert before buying your first home.

But if you understand these terms, the process usually feels less mysterious. A lot of the stress comes from hearing words you half-understand and trying to make big decisions around them.

Once you translate the jargon, it becomes easier to work out what problem you are actually dealing with.

- Are you borrowing-capacity limited?

- Are you cash-to-complete limited?

- Are you waiting on approval?

- Are you trying to understand the contract process?

Those are different problems.

The words matter because they help you work out which part is actually stopping you.