A lot of first-home buyer questions sound different, but they usually come back to the same few things.

Can I buy? How much cash do I need? Will the bank actually lend it? Which scheme applies? What am I missing?

So I thought I would put together the questions I get asked most often by first-home buyers.

This is general information, because lender policy, government schemes and state rules change. But it should give you a decent starting point.

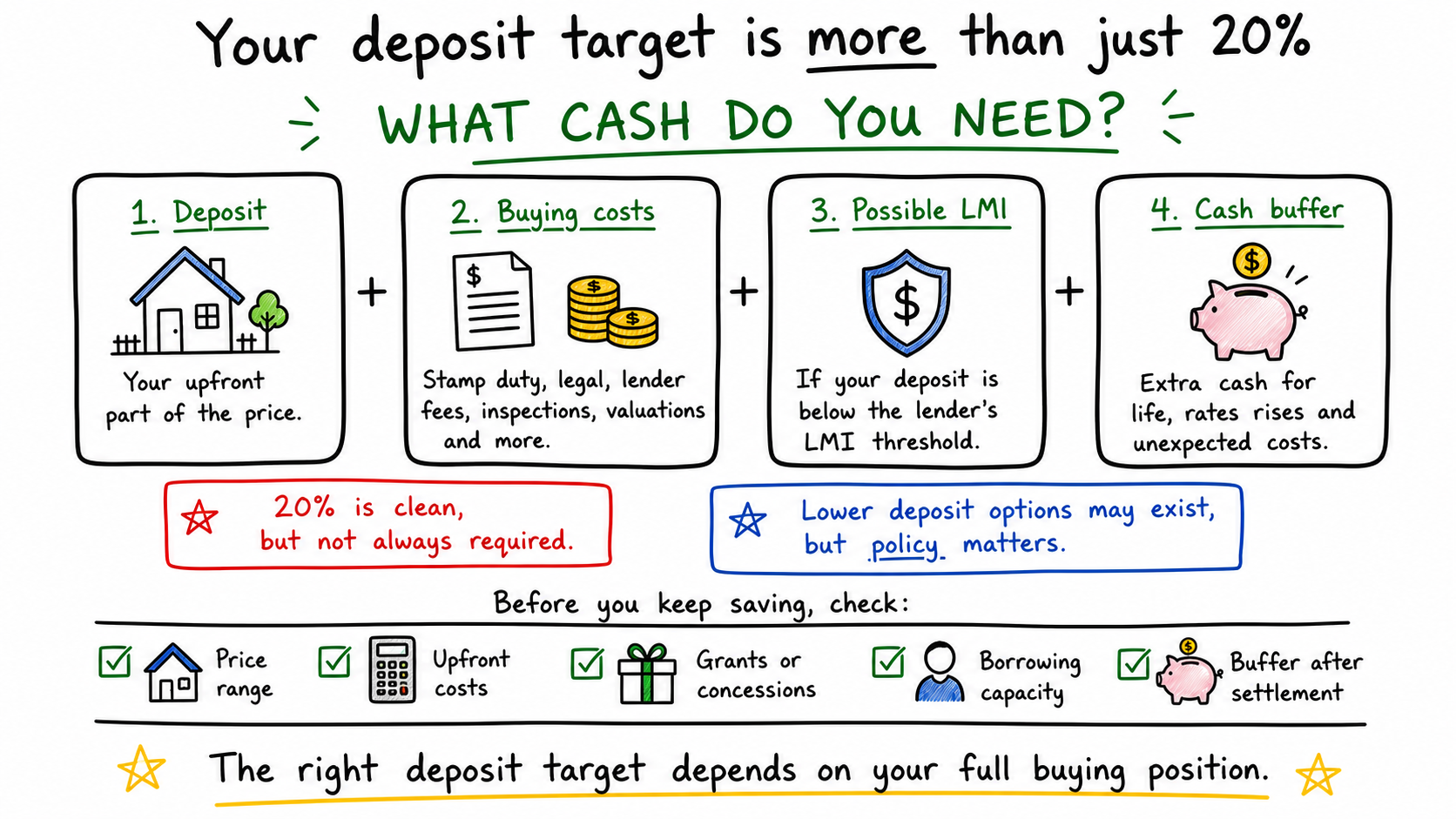

1. How much deposit do I actually need?

The annoying answer is: it depends.

The simple answer is that you need enough cash for three things: your deposit, your buying costs, and a bit of buffer after settlement.

A lot of buyers only think about the deposit. That is where they get caught out.

For example, if you bought a $700,000 property with a 5% deposit, that deposit is $35,000. But that does not mean $35,000 is all you need.

You might also need money for conveyancing, building and pest, bank or government registration fees, insurance, moving costs, rate adjustments and a bit of breathing room after settlement.

Also, a lower deposit does not magically solve borrowing capacity. If you put down 5% on a $700,000 purchase, you are still asking the bank for a $665,000 loan.

2. What actually stops first-home buyers from buying?

Usually one of two things. I think of it as two gates:

- Cash to complete.

- Servicing.

Cash to complete is whether you have enough money for the deposit, buying costs and buffer.

Servicing is whether the bank thinks your income can handle the loan.

Some buyers are deposit-limited. Some are servicing-limited. Some are both.

This is why two people can both say, "We want to buy for $750,000," but have totally different issues. One couple might have strong income but not enough savings. Another couple might have a great deposit but the bank still will not lend enough.

3. What do banks look at for borrowing capacity?

The bank is basically trying to answer one question: can you afford this loan without being cooked if things change?

They will usually look at your income, expenses, existing debts, dependants, credit history, deposit and the property itself.

They also assess the loan at a higher rate than the actual rate. That is the serviceability buffer. So if your real loan rate is around 6%, the bank may test your repayments at around 9%. That is why borrowing capacity can feel lower than expected.

You might look at your rent and think, "I already pay this much, why will the bank not lend me more?" The bank is not just looking at today's repayment. They are stress-testing you.

4. What is LMI and should I avoid it?

LMI stands for lenders mortgage insurance.

The annoying part is that it protects the lender, not you.

It usually comes up when you borrow more than 80% of the property value. So if you buy for $700,000 and borrow $665,000, your loan is 95% of the property value. That would normally be LMI territory.

Ways people avoid or reduce LMI can include:

- Using a government guarantee scheme, if eligible.

- Saving a 20% deposit plus costs.

- Using a family guarantee.

- Using a lender with profession-based LMI waivers, if you qualify.

Sometimes paying LMI is not automatically bad. If paying LMI gets you into the market years earlier, it might be worth considering. But it should be a conscious trade-off, not something you discover at the last minute.

5. Which government schemes are worth knowing about?

The main ones first-home buyers usually ask about are:

- The Australian Government 5% Deposit Scheme, formerly known as the Home Guarantee Scheme.

- Help to Buy.

- The First Home Super Saver Scheme.

- State-based grants and stamp duty concessions.

The trap is thinking all schemes solve the same problem. They do not.

The 5% Deposit Scheme mainly helps with the deposit and LMI problem. It does not mean the bank will lend you more.

Help to Buy is different. That is shared equity. The government contributes part of the purchase price, which can reduce the loan you need, but the government then owns part of the property value.

The First Home Super Saver Scheme is more of a savings strategy through super.

State grants and stamp duty concessions depend heavily on where you buy and whether the property is new or established.

For example, at the time of writing on 8 June 2026, eligible first-home buyers in Queensland may get strong stamp duty concessions under certain thresholds, but the rules are different depending on whether it is an established home, a new home, vacant land, and the purchase price.

6. What hidden costs should I budget for?

The deposit is the obvious one. The other costs are the ones that sneak up on people.

I have written a separate post on this topic that goes deeper into the hidden costs first-home buyers often forget.

But just to name a few common ones:

- Conveyancing or solicitor costs.

- Building and pest inspection.

- Bank fees, if applicable.

- Government registration fees.

- Transfer duty, depending on the state and your eligibility.

- Home insurance.

- Council, water and rates adjustments.

7. How do HECS, car loans and credit cards affect borrowing power?

They can matter a lot. A car loan is usually straightforward. The bank includes the repayment as an ongoing commitment.

Credit cards are annoying because lenders usually assess the limit, not just the balance. So even if you pay your card off every month, a $10,000 limit can still hurt borrowing capacity.

HECS or HELP is different again. It is not assessed like a normal personal loan, but it reduces your usable income because repayments come out through the tax system once your income is above the relevant threshold.

The main point is that debts reduce the income the bank sees as available for the home loan.

Sometimes closing or reducing a credit card limit can help. Sometimes paying out a car loan can help. Sometimes it makes no difference because something else is the bottleneck.

Again, it comes back to working out which part is actually stopping you.

8. Fixed or variable?

This is one of those questions where people want a perfect answer, but there usually is not one. A fixed rate gives you certainty. A variable rate gives you flexibility.

Fixed can be useful if you really want repayment stability and you are comfortable giving up some flexibility.

Variable can be useful if you want offset access, extra repayment flexibility, or the ability to refinance or sell without worrying as much about break costs.

A split loan is the middle-of-the-road option: part fixed, part variable.

The question is not just, "Which one could save me the most?" It is also, "Which mistake would hurt me more?" Some people hate uncertainty. Some people hate being locked in.

9. What is an offset account and do I need one?

An offset is basically a transaction account linked to your home loan. The money in the offset reduces the loan balance used to calculate interest.

Example: you have a $600,000 home loan and $30,000 in offset. The bank calculates interest as if the loan was $570,000.

That does not mean your repayment automatically drops. It usually means more of your repayment goes towards principal instead of interest. Offsets are great if you keep cash sitting around. They are also handy because you can keep money accessible while still reducing interest.

But they are not always free. Some loans with offsets have annual package fees or slightly higher rates. So if someone only keeps $1,000 in there, the offset may not be worth paying extra for.

Good feature. Not magic.

10. Do I need pre-approval before looking?

You do not always need it before casually browsing. But before you get serious, yes, I usually think it is a very good idea.

A pre-approval can help you work out:

- What budget is realistic.

- Whether your deposit works.

- Whether your income works.

- Whether any unusual policy issue exists.

- Which lenders may actually fit.

But pre-approval is not unconditional approval.

The property still needs to be acceptable. The valuation still needs to stack up. Your situation cannot materially change. The lender can still ask more questions. So treat pre-approval as a strong sense check, not a golden ticket.

Bonus: should I use a broker or a bank?

I am obviously biased here, because I am a broker and I do believe brokers can add a lot of value when they do the job properly.

Going straight to your bank can be fine if your situation is simple and that bank happens to suit you. The issue is that your bank only has its own policies and rates.

A broker can compare multiple lenders and work out which lender actually fits the scenario. That matters more than people think.

The cheapest-looking lender is not very useful if they will not approve the loan.

At the same time, brokers vary. Some are great, some are average, same as any industry.

The main thing I would look for is whether they can explain your situation clearly. Not just, "We can get you this interest rate."

More like:

- Here is your deposit position.

- Here is your borrowing capacity.

- Here is the likely bottleneck.

- Here are the trade-offs.

- Here is what I would fix before applying.

That is usually where the real value is.