As a mortgage broker, one of the biggest mistakes I see first-home buyers make is thinking they only need to save the deposit.

The deposit obviously matters.

But it is not the only cost of buying a home.

You might look at a $700,000 property and think:

5% deposit equals $35,000. So I need $35,000.

But that is not really the full number.

There are costs that sit on top of the deposit, and if you only find out about them once you are already making offers, it can be pretty demoralising.

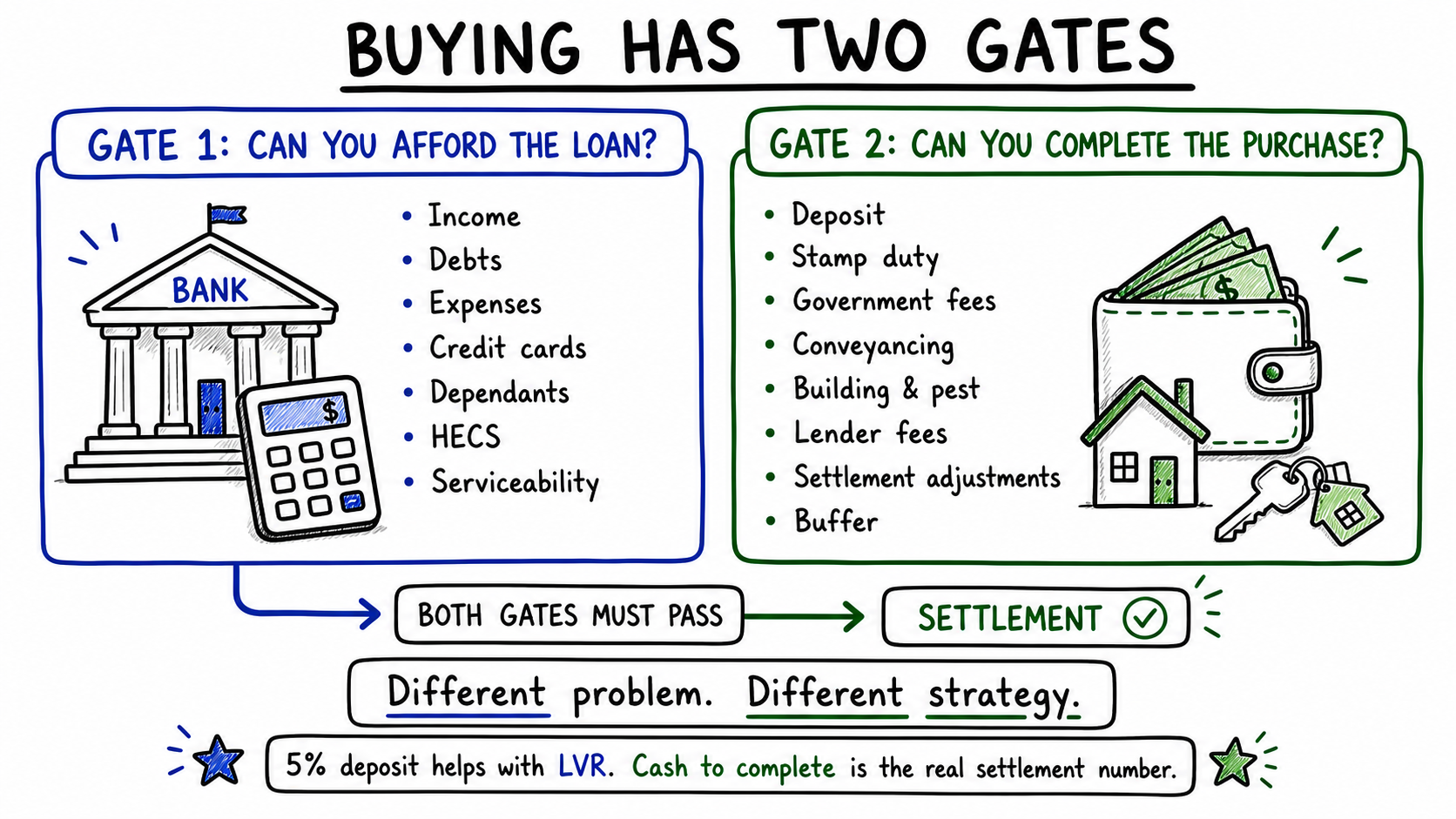

There are three buckets to think about

When you are working out the real number, it helps to split the costs into three buckets:

- Costs to buy the property.

- Costs around moving in.

- Costs after settlement.

Some of these are part of the loan approval conversation. Some are just part of real life. Both matter.

1. Costs to buy the property

Stamp duty

This is the big one.

Stamp duty, or transfer duty, is a state government cost charged when you buy property. Depending on where you buy and the purchase price, it can be a massive hit.

This is why first-home buyer stamp duty exemptions and concessions matter so much.

As a rough guide for buying existing properties, at the time of writing on 8 June 2026:

- Queensland: no transfer duty under $700,000 for eligible first-home buyers, with concessions above that and under $800,000.

- New South Wales: full exemption up to $800,000, with concessions above that and under $1 million.

- Victoria: full exemption up to $600,000, with concessions up to $750,000.

If you are building or buying a new property, the rules can be different and may be more favourable depending on the state, property type and purchase price.

So if you are eligible and buy under the relevant limit, stamp duty may be reduced or waived completely. That can save you a huge amount of money.

Conveyancing

Often around $1,500 to $2,500.

This is the legal side of the purchase. Contract review, searches, settlement and making sure the transfer is handled properly.

Building and pest inspection

Usually around $600 to $900.

Optional, but highly recommended. It checks for things like termites, structural issues and other defects before you go unconditional.

Mortgage registration and government fees

Usually a few hundred dollars.

Not the biggest cost, but still something that needs to be included.

Settlement adjustments

This one gets forgotten a lot.

At settlement, there may be adjustments for things like council rates, water rates or body corporate fees.

For example, if the seller has already paid council rates for the quarter, you may need to reimburse them for the portion that relates to your ownership period.

It is not usually the biggest number, but it can still be another few hundred dollars or more that buyers were not expecting.

2. Costs around moving in

This is the stuff that is not always part of the formal loan approval conversation, but still affects your actual life.

Building insurance

If you are buying a house, the bank will generally require building insurance to be in place before settlement.

This can vary a lot depending on the property, location, flood risk, construction type and insurer.

In Queensland, I commonly see quotes around $1,200 to $2,000+ per year, but it can be higher.

If you are buying a unit or townhouse, building insurance is usually included in the strata or body corporate fees instead.

Moving costs

Depends how much help you have.

It might be a van and a few mates. It might be a couple of grand for removalists.

Utilities and setup costs

Electricity, internet, gas if applicable, cleaning, small repairs, locks and random setup costs.

None of these are massive by themselves, but they add up.

Furniture and appliances

Very easy to underestimate, especially if you are moving out for the first time.

Fridge, washing machine, bed, couch, desk, blinds, lawn mower, basic tools.

You do not need to furnish the whole place on day one, but you probably want more than a mattress and a camping chair.

3. Costs after settlement

Your mortgage repayment is not the only cost of owning the home.

You may also have:

- Council rates.

- Water rates.

- Contents insurance.

- Strata or body corporate fees.

- Repairs and maintenance.

- Higher electricity bills.

- Emergency repairs.

This is where units and townhouses need a bit of extra attention.

Body corporate fees can vary massively. Sometimes they are a few hundred dollars per quarter. Sometimes they are thousands.

Lifts, pools, gyms, gates, large shared areas and older buildings can all change the numbers.

You want to know that before you buy, not after.

A rough example

Say you are buying a $700,000 home in Queensland as an eligible first-home buyer using a 5% deposit scheme.

A rough example might look like this.

Cash needed to settle

- Deposit: $35,000.

- Stamp duty: $0 if eligible.

- Conveyancing: $2,000.

- Building and pest: $750.

- Mortgage registration and government fees: $300 to $500.

- Settlement adjustments: maybe $500 to $1,500.

So your settlement number might be closer to $39,000 to $40,000+.

But that still is not the full practical number.

Cash needed around moving in

- Building insurance: maybe $1,200 to $2,000+ per year.

- Moving costs: $500 to $2,000.

- Utilities and setup: a few hundred dollars.

- Furniture and appliances: depends massively.

- Immediate repairs and hardware runs: almost always more than people expect.

So while the deposit is $35,000, the real-world amount you want available might be more like $45,000 to $50,000+.

And that is before we even talk about keeping a proper safety buffer.

Ask for the full number early

None of this is meant to scare people away from buying.

It is just something you want to know early.

Because the worst time to find out you need extra money is after you have already made an offer and emotionally moved into the place in your head.

So if you are a first-home buyer, do not just ask, "How much deposit do I need?"

Also ask, "What are all the extra costs I need to budget for?"