One of the most common scenarios I talk through with clients is:

"We want to sell our current place and buy the next one. How do we actually make that happen?"

It sounds simple, but there is a fair bit of nuance in it.

When you are buying your first home, the process is usually cleaner. You have your deposit, you work out your borrowing capacity, then you buy.

When you already own a home and want to move, the strategy depends heavily on the order of operations.

That is usually the first thing I want to work out.

Why the order matters so much

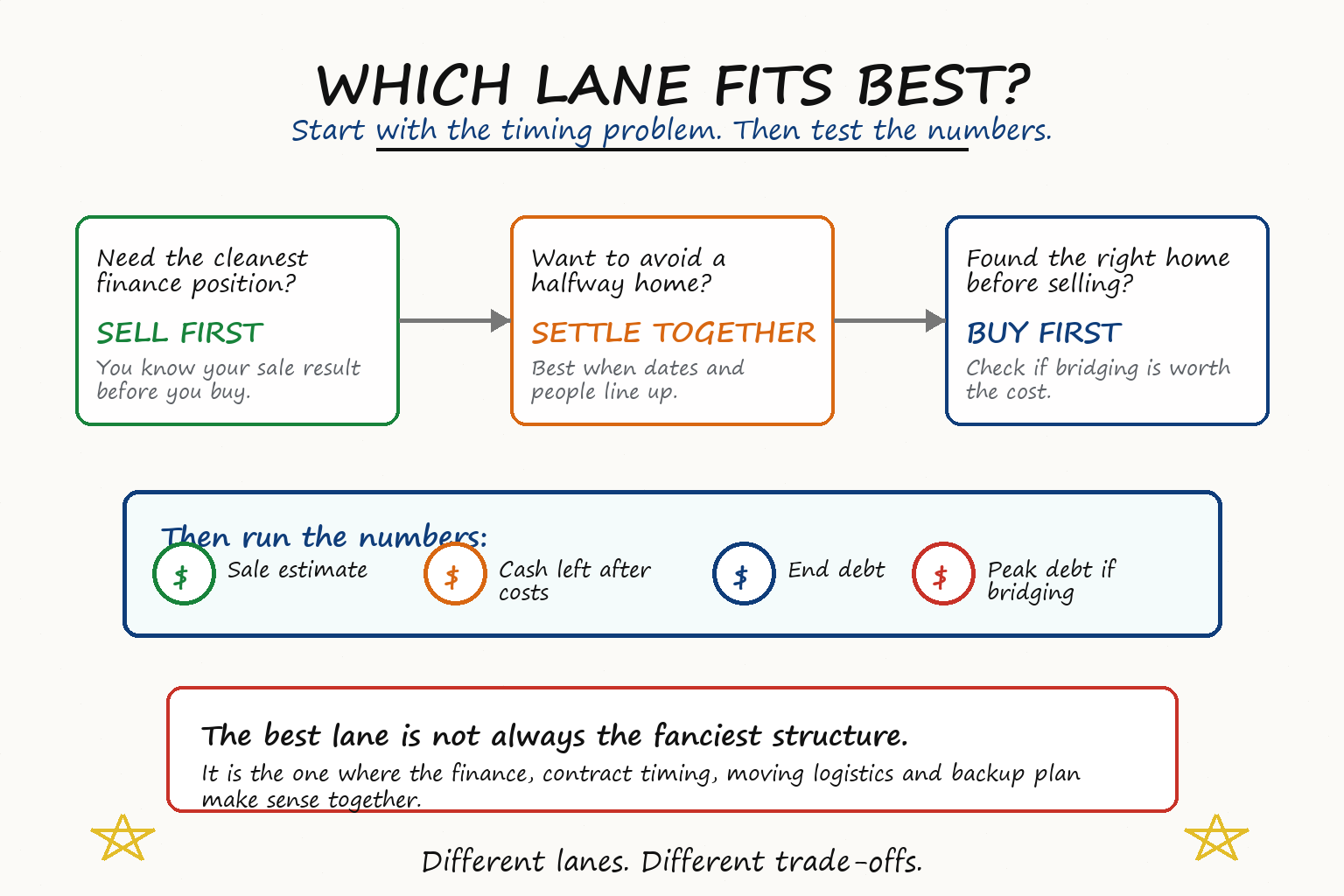

Most people start by asking what loan product they need. That is understandable, but it is usually not the first question.

The better starting point is: what happens first?

If you sell first, your equity becomes real cash before you buy. If you settle both properties together, the sale proceeds need to flow into the purchase at settlement. If you buy first, you may need short-term finance to hold both properties until the old one sells.

Same goal. Very different finance conversations.

Option 1: Sell first, then buy

This is usually the cleanest option financially.

You sell your current home, pay out the existing loan, work out how much cash you have left, then go and buy the next place with a normal home loan.

From a lending point of view, there is nothing too fancy going on. You know your deposit. You know your debt. You know what loan you need.

The trade-off is the life admin.

You may need somewhere to live in between. You may need to move twice. You may need storage. You may be staying with family. You may be sitting there with cash in the bank, waiting for the right property to come up.

This can be a really sensible way to do it if you have flexible timing, family you can stay with, a short-term rental option, or you do not mind being in limbo for a bit.

It can also give you more certainty when you are making offers, because you know what your sale has actually achieved rather than working off estimates.

Option 2: Sell and buy on the same day

This is called a simultaneous settlement.

Your sale settles and your purchase settles on the same day. The proceeds from your sale are used towards the purchase, and everyone tries to make the timing line up.

When it works, it can be a great balance. You avoid the halfway-home problem, and the finance can still be fairly straightforward.

Sometimes it is just a normal new loan. Sometimes, depending on your lender and the structure, you may even be able to look at something like a substitution of security or loan portability. That is where the lender releases the old property as security and takes the new property instead.

That can be useful if you have a good existing loan structure, a fixed rate, or some other reason you do not want to completely pay out the loan and start again. It is not automatic though. The lender still needs to approve it, and the new property and loan position still need to fit policy.

But the catch is obvious.

You need the stars to align.

The buyer of your property, the seller of the new property, both solicitors or conveyancers, both banks, the settlement platform, settlement dates, removalists and agents all need to do their part.

A simultaneous settlement can be neat on paper and stressful in real life.

You also need to think about offer strength. If your purchase offer is subject to the sale of your current property, the seller may see it as less attractive than a cleaner offer. Not always a dealbreaker, but it matters.

Option 3: Buy first, then sell

This is where bridging finance usually comes in.

A bridging loan can let you buy the new property before selling your current one. In plain English, it helps cover the gap between paying for the new home and receiving the sale proceeds from the old home.

This is usually the most convenient option from a lifestyle point of view.

You can buy the right property when it comes up. You can move in. You can take your time preparing the old property for sale. You are not trying to move out, sell, buy and settle all at once.

But it is normally the most expensive option.

The reason is pretty simple: for a period of time, you are holding a lot more debt than you actually want to end up with.

Peak debt and end debt

This is the part people often miss.

With bridging, there are really two debt numbers.

Peak debt is the big ugly number while you own both properties. It is usually the point where the lender's exposure is highest.

End debt is the loan you are left with after the old property sells and the sale proceeds have been used to reduce the debt.

The end debt might be completely fine.

The peak debt might look disgusting.

That is why bridging needs to be thought through properly. It is not just "can I afford the final loan?" It is also "how expensive and risky does the middle part get?"

That time can be valuable.

It might let you avoid panic-selling. It might let you clean up, style or stage the old property properly. It might let you buy the right home without making a weaker subject-to-sale offer. It might help you avoid two moves.

But that time is not free.

If the bridge is only open for a short period, the cost may be manageable. If it drags out for months, it can get expensive quickly.

Do not just stare at the interest number

It is easy to look at a bridging cost estimate and have a mild emotional event.

Fair enough. Sometimes the number is not pretty.

But the better question is: what does that cost actually allow us to do?

If bridging costs $20,000, but the extra time helps you avoid rushing the sale and you sell for $50,000 more, the conversation changes.

If bridging costs $40,000 and the old property sits there for months with no real upside, that is a different conversation.

No crystal ball, obviously. But that is the trade-off.

What lenders usually want to see

Bridging policy varies between lenders, so this is not a one-size-fits-all checklist. But there are some themes that come up a lot.

- How much equity you have in the current property.

- What the peak debt looks like compared with the combined property values.

- Whether the expected end debt is affordable after the old property sells.

- How realistic the sale estimate is for the existing property.

- Whether the old property is already listed, under contract, or still being prepared for sale.

- How interest during the bridge will be paid or capitalised, depending on lender policy.

- What the backup plan is if the sale takes longer or comes in lower than expected.

That last point matters. A good bridging conversation should include the boring-but-useful questions. What if the property takes six months to sell? What if the sale price is lower than expected? What if rates or repayments move? What if the lender will only assess the deal in a certain way?

Those are not fun questions. They are the questions that stop the structure from being built on wishful thinking.

Other ways to solve the timing problem

Bridging finance is not the only option. Sometimes the better answer is just a cleaner contract or settlement strategy.

- A longer settlement on your sale so you have more time to find the next property.

- A longer settlement on your purchase so you have time to sell.

- A subject-to-sale clause, where the purchase depends on your sale happening.

- Renting back your current property from the new owner for a short period after settlement.

- Negotiating early access or delayed possession, with proper legal advice.

- Keeping the existing loan through a security substitution, if the lender and settlement timing allow it.

- Buying a tenanted property and holding it as an investment for a while before moving in later.

Some of these are finance questions. Some are legal or conveyancing questions. Some are negotiation questions.

The point is not to force every move into a bridging loan. The point is to work out which timing problem you actually have.

A practical checklist before you choose a lane

- What is the realistic sale range for your current property?

- How much debt will be paid out when it sells?

- What cash will be left after selling costs, loan payout and purchase costs?

- Can you service the end debt comfortably?

- If buying first, what is the estimated peak debt?

- How long could you carry the bridge if the sale takes longer than expected?

- Would a longer settlement or rent-back arrangement solve the same problem more cheaply?

- Will your offer be stronger or weaker depending on the structure?

- Have your broker, conveyancer and agent all looked at the same plan?

So which option is most suitable?

There is no universally suitable option. There is only the version of the mess you are most comfortable with.

Selling first usually gives you cleaner finance but messier logistics.

Same-day settlement can be a good balance, but the timing has to work.

Buying first with bridging finance can give you more control and convenience, but the temporary debt and interest cost need to be worth it.

The goal is not to find the fanciest structure. The goal is to work out the order of operations, then match the finance strategy to that order.

Different lanes. Different trade-offs.

Frequently asked questions

Is bridging finance only for people who have not sold yet?

Usually, yes. In a standard move, bridging finance is used when you need to buy the new property before the old one has settled. If your current property has already sold and settled, you may not need a bridge because the sale proceeds are already available.

Do you pay two home loans during bridging?

It depends on the lender and structure. Some scenarios involve paying interest during the bridging period, while some lenders may allow interest to be capitalised. Either way, the cost is real and should be modelled before you commit.

Can I keep my current loan when I move?

Sometimes. This is usually called substitution of security, loan portability or a security swap. The basic idea is that the loan stays in place and the property securing it changes. It is subject to lender approval, property security requirements and settlement timing.

Is a subject-to-sale offer a bad idea?

Not always. It can protect you from being locked into a purchase before your sale is secure. But it can also make your offer less attractive to a seller, especially if they have cleaner offers on the table.

What should I do first?

Before you start inspecting properties seriously, map the three lanes with actual numbers. Sale estimate, existing loan, cash left after sale, purchase budget, end debt, possible peak debt and timing risk. Once those are on one page, the decision usually becomes much clearer.