If you are looking to buy your first property, or your next one, you have almost certainly been told to get pre-approval. But what is it really, and when should you get it?

What pre-approval actually is

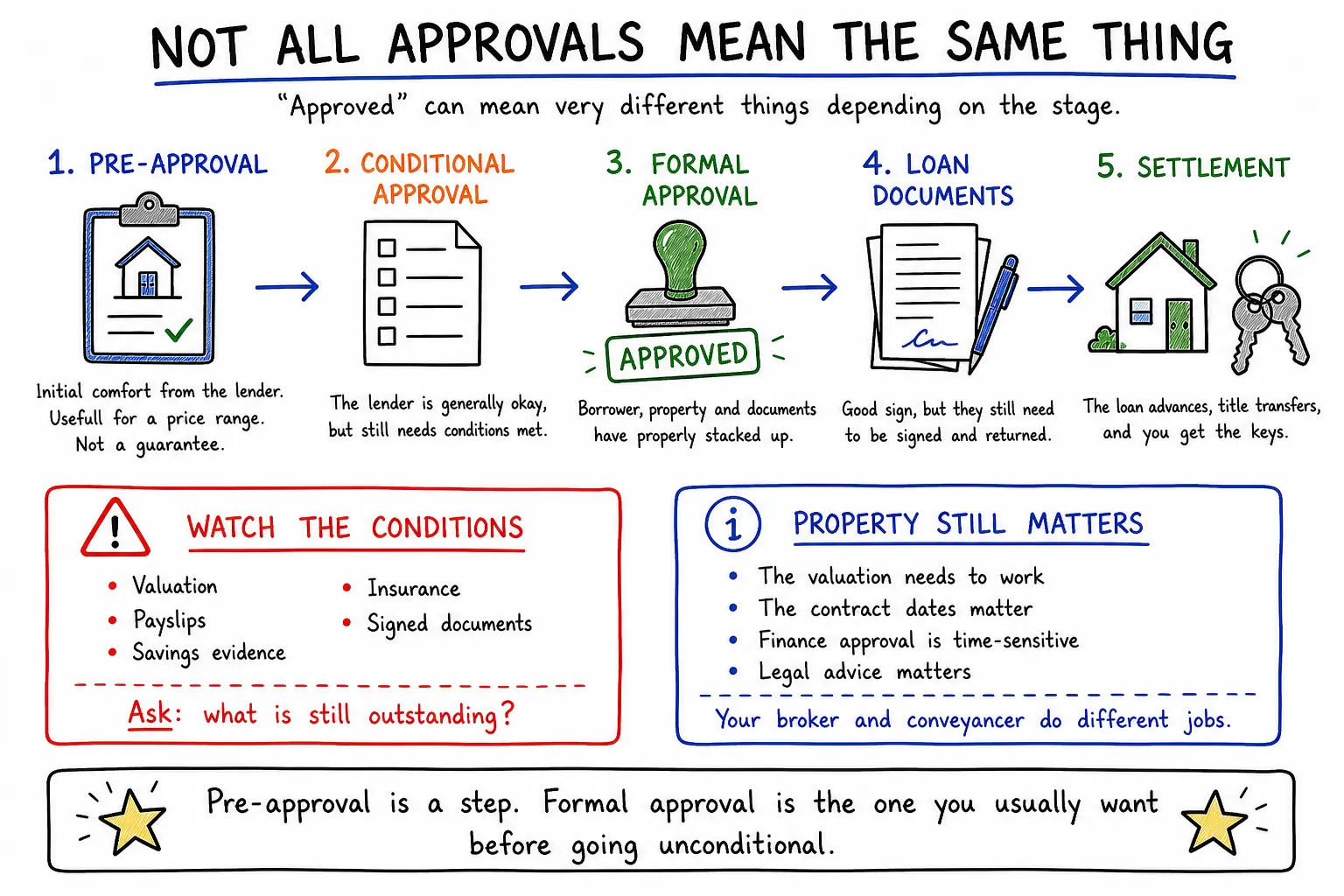

Pre-approval is an indication from a lender that, based on your income, debts, expenses and deposit, they are willing to lend you up to a certain amount at a certain loan-to-value ratio. It does not mean you have the loan. It means you know what price range you can seriously look at.

The one variable missing is the property. That is the main difference between pre-approval and approval. When you find a place and the lender is happy the property meets their policy and valuation, the application moves from pre-approval to full approval.

Pre-approval is not a guarantee

Two pre-approvals can look identical and mean different things. Some lenders run automated system pre-approvals: fast, convenient, and fine for simple situations, but nobody has actually looked at your file. Others do fully assessed pre-approvals, where a credit assessor reviews everything before greenlighting it. If your situation is complex, self-employed income, recent job change, unusual property plans, a fully assessed pre-approval is worth a lot more.

Either way, the property side is still to come. The valuation happens after you have signed a contract, which is exactly why bidding unconditionally at auction on the strength of a pre-approval carries risk. I wrote about that separately in the auction article.

Why get pre-approved at all

- Faster finance when it counts. The lender already has your details, so the gap between offer and formal approval shrinks. That lets you put a shorter finance clause on your offer, which many sellers value more than a slightly higher price with a long clause.

- You stop guessing your ceiling. Without pre-approval, you can put an offer on a property you believe is in range and find out it is not. That costs you the property and sometimes a deposit-sized headache.

- You make lender decisions early. Choosing where to get pre-approved is really choosing your lender shortlist: who suits your LVR, your income type and the features you want.

The process

Applying for pre-approval looks like applying for any home loan. You and your broker put together your deposit, income and expenses, and the application goes to the lender as a kind of mock application, assessed under the same policy the real one will be. If your circumstances change after pre-approval, new debts, changed job, different deposit, tell your broker, because the pre-approval was issued on the old facts.

How much should you apply for?

It depends on the LVR you are targeting, which is really a deposit question. If your numbers support a $600,000 purchase at 80% LVR or a much bigger purchase at 90% with LMI, and you only want to look at properties under $600,000, the 80% pre-approval is the cleaner tool. If the properties you actually want start at $750,000, you need the higher-LVR pre-approval and the costs that come with it.

Different lenders have different sweet spots. Some are strong at high LVRs because of LMI waivers for certain professions or schemes; others price hardest for low-LVR borrowers. If you change your mind later, you can adjust the amount or move the pre-approval to another lender. As a rule of thumb: apply for the maximum you can service at the LVR you are targeting, for the price range you genuinely intend to shop in.

When to get it

When you are ready to start hunting. Pre-approvals expire, typically after around three months depending on the lender, so getting one six months before you are ready mostly guarantees you will do it twice.

And if your purchase is already locked in, say a private sale from family, you may not need pre-approval at all. Your broker will still assess whether you can borrow the amount, but the pre-approval itself is a shopping tool, and you are not shopping.

Does applying hurt your credit score?

This came up when I posted this on Reddit, and it is a fair question. A pre-approval application generally involves a credit enquiry, and a pile of enquiries in a short window can read as credit stress to lenders and scoring models. One or two spaced-out enquiries are normal and expected for someone buying a home.

The practical answer: do the numbers work with your broker first, without lodging anything. Lodge the pre-approval when you are actually ready to shop, and renew it deliberately rather than re-applying on autopilot every time one lapses.

What to do next

If you are within a few months of seriously looking, get the assessment conversation going now and the pre-approval lodged when the hunting starts. If you are further out, spend the time on the two numbers that decide everything anyway: your deposit and your borrowing power. They are not the same thing.